Asset Identification

This has to be done thoroughly to ensure that each and every asset is identified. If the correct processes are followed, it would not be necessary to repeat this afterwards.

Because of the expense involved, it is generally avoided, which means that any of the steps that follows is lacking subsistence, and, essentially, meaningless.

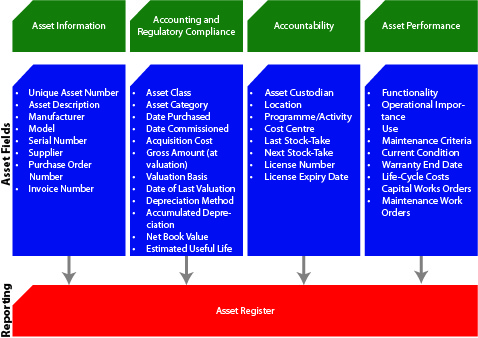

The Asset Register is a key to understanding in detail what assets are owned and controlled and, depending on the complexity of information entered, can be used to determine:

- The likely current condition of assets;

- When assets need to be replaced;

- Information required in meeting accounting standards and other regulatory requirements;

- Asset locations and asset custodians for stock-takes;

- The level and frequency of asset maintenance programs; and

- Life-cycle costs by asset, program and business activity.

|